Citibank Asia has been one of the most innovative banks in the region, especially with regards to credit cards. Today, I will review the different credit cards Citibank Philippines offers, compare their benefits and fees and will recommend the best general, everyday credit card – of course with an eye on rewards!

While a lot of people envy the US for all the great credit card offers, Citibank Asia has offered travel rewards cards for years, including the option to transfer points to airline partners. In fact, it appears that Citibank US leveraged the relationships in Asia to introduce transfer partners in the ThankYou points program: The list of partners is heavily geared towards the leading Asian carriers, who have been available in Asia for a while! So, let’s look at the cards currently available through Citibank Philippines. I recently became a customer of Citibank in Manila. As a Citigold customer in the US, I receive the same level of service in the Philippines, including a fee waiver for one credit card, so I wanted to pick the best one!

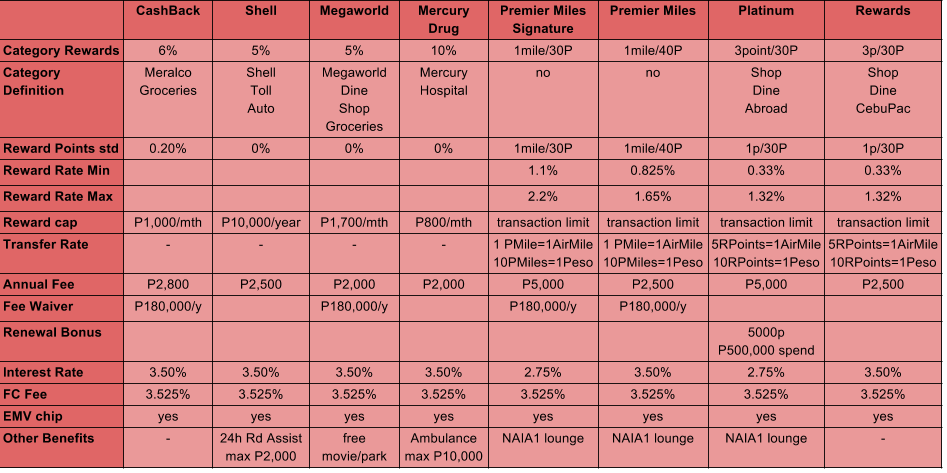

Citibank PHL currently offers 8 credit cards, 4 of them offer discounts in specific categories, like groceries or drugs, and 4 have their own point currencies that can be used for rewards or transferred to partners. All of the cards now have chip technology for security, carry an annual fee, charge a hefty foreign exchange fee and a, compared to the US, reasonable interest rate! None of the cards offer a sign-up bonus that make rewards cards so popular in the US. Here are all the options in comparison:

The rewards cards sound great in the advertisement, offering discounts of up to 10% – which is higher than anything you can get in the US. Unfortunately, the devil is in the details and after reading through the terms and conditions (so much fun! Right!), those discounts started to wither away:

The Citi Cashback card offers a 6% discount on groceries, 2% on Meralco (electricity, in the heat of Manila, a big monthly bill, thanks to your air conditioner) and 0.2% on everything else. Unfortunately, you need to spend at least P10,000 in non-bonus categories to earn these discounts or the category bonus drops to the standard 0.2%. This means, you can’t really get this card in addition to your day-to-day card just for the bonus categories. That really makes the card difficult to use effectively. To make it worse, the category bonus is capped at P1,000/month (or $22) – that’s hardly worth the effort! You can get the annual fee of P2,800 with an annual spend of P180,000 – that’s a better discount than the cashback!

The Citi Shell card is very similar in set-up: With a minimum monthly spend of P10,000 in non-category spend, you earn a 5% bonus on Shell fuel, road tolls and auto shop bills, but no discount on anything else. Without that minimum spend, you only get 3% at Shell. Your total reward is capped even lower – at P10,000 for the year! There is no fee waiver mentioned, but it might be possible to request similar to cashback card. An extra benefit is Roadside Assistance – up to a maximum of P2,000/year, basically once a year for limited help!

The Citi Shell card is very similar in set-up: With a minimum monthly spend of P10,000 in non-category spend, you earn a 5% bonus on Shell fuel, road tolls and auto shop bills, but no discount on anything else. Without that minimum spend, you only get 3% at Shell. Your total reward is capped even lower – at P10,000 for the year! There is no fee waiver mentioned, but it might be possible to request similar to cashback card. An extra benefit is Roadside Assistance – up to a maximum of P2,000/year, basically once a year for limited help!

The Citi Megaworld card is next to follow this pattern – with a minimum non-category spend of P15,000, you earn 5% on dining, shopping and groceries at Megaworld malls, nothing on other spend. If you fall below the spend treshold, you earn 5%, 3%, 1% respectively. Your rewards are capped at P1,700/month and you can get your annual fee of P2,000 waived with a spend of P180,000. An unusual perk is that for every transaction of more than P2,500, you get a free movie (up to P200) or parking pass (approx P45).

The Citi Mercury card combines the highest banner-rate discount of 10% on Mercury drugs and partner hospitals with the lowest reward cap of only P800/month! You also need a minimum spend of P10,000 in other categories to receive it – or your discount drops to 5% at Mercury and 2% at hospitals. The unique benefit of this card is the use of an ambulance in emergencies – up to P10,000/year.

All four of these cards make for great advertising posters with high discount percentages – but the fine print, conditions and earning limits make these cards more work than they are worth. You can have them as secondary cards for the specific categories, but then need to pay attention to getting the non-category spend. If you can afford multiple cards and spend limits, your time is probably worth more than the rewards you will get…That brings us to the more generic rewards cards with transfer partners.

First, you have the Citi Rewards and Citi Platinum cards. They both use the “Rewards Points” currency and earn 1 Reward Point for every 30P spent. In addition, the Citi Rewards card will earn 3 points/30P on shopping and dining in the Philippines as well as on Cebu Pacific tickets. The Platinum card earns 3points/30P for shopping and dining in the Philippines as well as all spend abroad. Keep in mind that the foreign exchange fee is still 3-10x higher than what the reward points are worth, so you are still better of with cash or a no-fx-fee credit card outside the Philippines. You also get a 5,000 point bonus for an annual spend of P500,000 as well as access to the airport lounge at NAIA Terminal 1 with the Platinum card. The Rewards Points you earn with both cards can be used like cash at a rate of 10 points for P1 cash or transferred at a rate of 5 points for one airline or hotel mile. The points-for-cash rate is horrible, the equivalent of a 0.33% rebate, so you are much better of to use your points for transfers, which can get you around a 1.32% rebate, if points are used wisely!

Last but certainly not least are the two Premier Miles cards. The basic Premier Miles card earns miles at a rate of 1 point for P40 spend (or a reward rate of 0.825%-1.65%), while the Premier Miles Signature card earns points at a rate of 1point/P30 spend, increasing the reward rate to 1.1%-2.2%. There is no limit for the number of miles you can earn every year, but there is a transaction limit (so you can’t buy a car or house with the card!). The latter card also carries the typical benefits of an Visa Signature card and a lower interest rate of 2.75% (versus 3.5%). Those higher rewards and benefits come at an annual fee of P5,000 compared to P2,500 of the basic card. While it is not stated on the web site, I remember from my own application that those annual fees can be waived with an annual spend of P180,000 – or a Citigold membership. The best thing about these cards though is the ability to transfer Premier Miles at a ratio of 1:1 to hotel and airline partners. In addition to the flag carrier, Philippine Airlines, you have some of the world’s best airlines in the program, like Singapore Airlines, Cathay Pacific and Thai Airways. With partners like British Airways, Etihad and Delta you get global reach. The list is made complete with airline partners Garuda, Malaysian Airlines, Eva Air and hotel partners Hilton and IHG! These partners make the Citibank cards very attractive and the 1:1 transfer ratio makes the Premier Miles cards superior to the Rewards/Platinum cards!

Last but certainly not least are the two Premier Miles cards. The basic Premier Miles card earns miles at a rate of 1 point for P40 spend (or a reward rate of 0.825%-1.65%), while the Premier Miles Signature card earns points at a rate of 1point/P30 spend, increasing the reward rate to 1.1%-2.2%. There is no limit for the number of miles you can earn every year, but there is a transaction limit (so you can’t buy a car or house with the card!). The latter card also carries the typical benefits of an Visa Signature card and a lower interest rate of 2.75% (versus 3.5%). Those higher rewards and benefits come at an annual fee of P5,000 compared to P2,500 of the basic card. While it is not stated on the web site, I remember from my own application that those annual fees can be waived with an annual spend of P180,000 – or a Citigold membership. The best thing about these cards though is the ability to transfer Premier Miles at a ratio of 1:1 to hotel and airline partners. In addition to the flag carrier, Philippine Airlines, you have some of the world’s best airlines in the program, like Singapore Airlines, Cathay Pacific and Thai Airways. With partners like British Airways, Etihad and Delta you get global reach. The list is made complete with airline partners Garuda, Malaysian Airlines, Eva Air and hotel partners Hilton and IHG! These partners make the Citibank cards very attractive and the 1:1 transfer ratio makes the Premier Miles cards superior to the Rewards/Platinum cards!

While the research and comparison wasn’t easy, given the mountains of terms, conditions and fine print, my decision in the end was very easy: The Premier Miles Signature card offers the best reward value with no earning limit or complicated conditions, making it easy to use as an everyday card and rewarding with the great airline partners. I’m a big fan of Singapore Airlines and Thai Airways and I’m sure the Premier Miles will provide me a great flight at some point in the future! I will provide a more detailed report on my Citibank Premier Miles Signature Visa card soon! Before you sign up for any credit card, please make sure to read “How we evaluate credit cards“! You can find all the latest details directly at Citibank!

Totally agree on this. I currently have the premiermiles card as my 2nd citibank card. And I’m a bit worried with the annual fee. Is it stated in the fine print that if you spend at least 180k per year and the annual fee will be waived?

My first card with citibank is the rewards card and I got the no annual fee for life promo so no worries there.

I remember the fee waiver based on spent of 180k as you describe from when I applied. I checked the current terms & conditions on the Citibank website and they don’t provide that detail anymore. I’d assume that you would be grandfathered under the rules you signed up for, but would recommend you confirm by calling them.