United just launched a mileage earning pre-paid Visa card in partnership with Netspend. You earn miles in the MileagePlus rewards program, without the risks of a credit card – is this a good deal for travelers? Not really, the card has high fees that eat up all/most of the value you’d get from the points, leaving you with better alternatives for most people. Find out who can benefit from this card – and who won’t!

I have previously recommended prepaid card for travelers to manage the risk of using credit cards in high-fraud countries or transactions, like the American Express Bluebird or Simple Visa. Both limit the risk of fraud to the balance of your pre-paid card and give you peace of mind, so you don’t have to spend your trip on the phone trying to block your credit card or recover money from fraud!

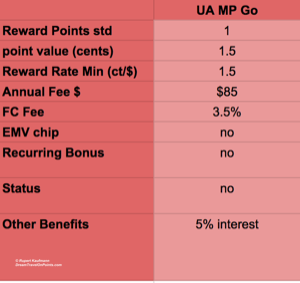

Features: The MileagePlus Go Visa card is the only pre-paid card in the US to earn airline miles. You earn 1 mile for $1 of spend with signature transactions processed as “Credit” (not PIN transactions), up to $2,500 per month (or $30,000 per year).

Features: The MileagePlus Go Visa card is the only pre-paid card in the US to earn airline miles. You earn 1 mile for $1 of spend with signature transactions processed as “Credit” (not PIN transactions), up to $2,500 per month (or $30,000 per year).

Another unique feature for a prepaid card is the interest of 5% paid on balances up to $1,000 – that’s basically a high-interest savings account!

Similar to other cards, you can manage your money with a mobile app, including loading checks, see transactions or mileage earned. It lacks some of the features AmEx or Simple offer, like a set-aside account or setting goals.

The card has FDIC insurance like a checking account and fraud insurance like a credit card – in addition to limiting the risk via the prepaid balance.

Fees: The unique opportunity to earn points comes with steep fees similar to other prepaid cards offered by Netspend. There is a long list (read the fine print here), but the most important ones are:

– Annual fee: $85

– Foreign Exchange Fee: 3.5%

– Foreign ATM Fee: $4.95 + fx fee

In comparison, neither AmEx Bluebird or Simple charge an annual fee. AmEx doesn’t charge an FX fee and Simple has a much lower fee of 1%. BlueBird can’t be used at foreign ATMs any longer and Simple doesn’t charge a fee there!

But, can the points and interest make up for the fees? Let’s do the math:

Balance of $1,000: $50 interest per year

Monthly US spend of $200: 6,000 miles/year, a value of $36

Monthly US spend of $2,500: 30,000 miles/year, a value of $450

So, if you carry a balance of $1,000 and spend at least $200 in the US, you card is essentially free, but you haven’t earned a single mile yet. That puts you even with the AmEx Bluebird or Simple Visa.

If you max out the mileage earning potential, the card will generate $415 of benefits with a spend of $30,000 – that’s 1.4% earn rate. While that’s not a great earn rate, it’s better than any other prepaid card and many credit cards!

For anybody who can qualify for premium credit cards, the United MileagePlus Explorer card offers a sign-up bonus of 50,000 points, higher earnings and perks like priority boarding, free checked bags and no fx fee! My favorite travel card, the Citibank Prestige, can earn even higher rewards and more perks!

Who’s the card for?

The Unbanked: Most prepaid cards target the “unbanked” in the US. Depending on which study you read, that’s anywhere between 8-25% of the US population who are relying on cash, cash checking and money orders – all much more expensive than even this prepaid card.

The MileagePlus Go card does offer some benefits to that audience, by combining a checking account, savings account and rewards card into one! But you’ll have to manage your balance and spend so carefully to make it work (and not be stuck with the high fee) – I don’t think it’s worth the effort.

Instead, if you can’t get a credit card, I’d recommend to use Simple to manage your money. It helps to set goals, manage budgets and help you save some money. The app is much better and it’ll be much easier to manage! In parallel, you can work on improving your credit by applying for basic credit cards or store credit cards first.

Peace-of-Mind-Travelers: If you are looking to manage your risk in high fraud situations, the high FX fees and foreign ATM fees destroy any possibility of earning a reward with this card. It will outstrip the points value by more than 2x, so this card does not make much sense for somebody using it to manage risk abroad! Look at the AmEx Bluebird or Simple Card instead. I consider the general fraud risk in the US pretty low for credit card transactions, so there is little to gain from a prepaid card when traveling in the US!

Bottomline: While the MileagePlus Go Visa card has some intriguing features, like the 5% interest and points earning potential, the high fees destroy most of that value. It’s too expensive to manage your fraud risk abroad as well as for most unbanked. Only if you belong to a niche of the unbanked who frequently travel on United, manage their balance tightly, have a pretty high monthly spend and don’t plan on improving their credit, need you apply. If that’s you, you can find out more here! Everybody else should look elsewhere! And before you do, read how we evaluate and recommend credit cards!